Trump’s Push to Ban Large Institutional Investors

Most people are reacting emotionally to the idea of Trump banning large institutional investors from buying single-family homes, without understanding what that actually means for prices, rents, and opportunity. This isn’t a “good vs evil” story. It’s a trade-off story. And trade-offs always create winners and losers.

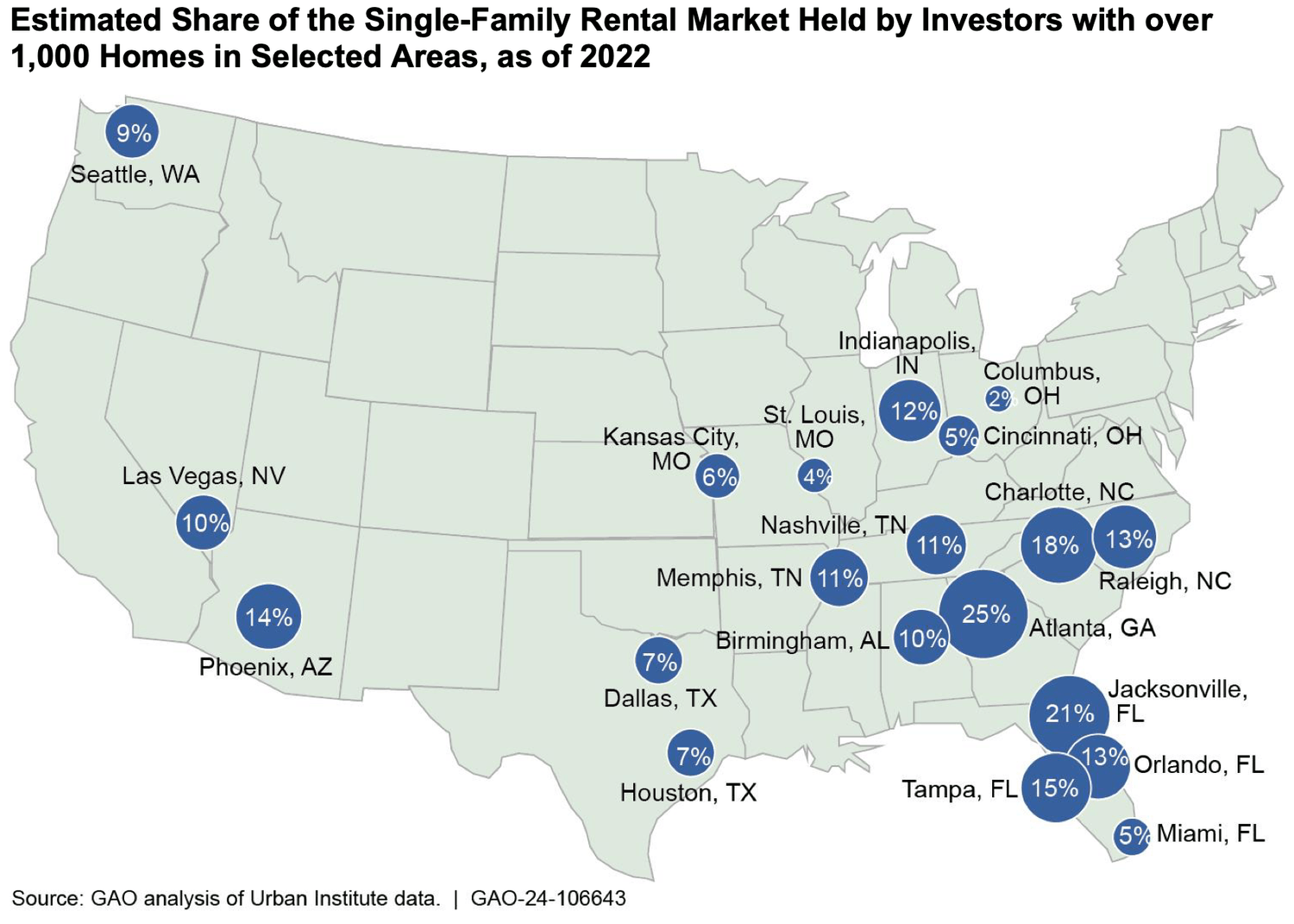

The proposal to restrict or ban large institutional investors from owning single-family homes has reignited a heated debate in U.S. housing policy. Under most definitions, these “institutional investors” are firms that own 1,000 or more single-family properties—Wall Street–backed entities often blamed for rising home prices and rents.

But the real impact of such a policy is more complex than the headlines suggest.

The Scale Problem: Small National Share, Massive Local Impact

Nationally, institutional investors own only about 3% of all single-family rental homes. That statistic is often used to dismiss their influence.

That’s misleading.

In certain Sunbelt markets, institutional ownership can reach 20–25% of the local rental stock. In those neighborhoods, these firms don’t just participate in the market—they shape it. That concentration is where policy intervention starts to make economic sense.

Potential Upside: Pressure Relief on Prices and Rents

Research consistently shows that in areas where institutional buying is concentrated, home prices and rents rise faster.

Why?

These firms remove homes from the resale market more permanently than mom-and-pop investors.

Their scale gives them pricing power, especially on rents.

Consolidation reduces competition among landlords.

Restricting large-scale institutional activity in targeted markets could reduce upward pressure on prices and rents, especially for entry-level homes that individual buyers are trying—and failing—to access.

Homeownership Could Expand—But Not Automatically

One of the strongest arguments for regulation is that it could shift housing stock back toward ownership.

The “build-to-rent” model is a prime example. Entire communities are now being developed specifically as rental neighborhoods, often with institutional backing. The Federal Housing Finance Agency has openly criticized this model because those same homes could be sold to owner-occupants instead.

Limiting institutional participation could leave more new and existing homes available to individual buyers—if financing, credit access, and affordability issues are addressed at the same time. Otherwise, supply alone won’t solve the problem.

The Uncomfortable Truth: Who Fixes the Worst Homes?

Here’s the part most people ignore.

A significant share of institutional investment targets distressed properties—homes needing $15,000 to $39,000 in repairs. Most individual buyers simply cannot:

Finance that level of renovation

Absorb the risk

Execute the work efficiently

Institutional investors can. They bring capital, systems, and speed.

Remove them entirely, and many of these properties don’t magically turn into starter homes. They sit vacant longer, deteriorate further, and drag down neighborhoods. Any serious policy must address who steps in to rehabilitate these homes if institutions are pushed out.

Rental Supply and Access: The Trade-Off No One Wants to Admit

Another inconvenient fact: 85% of renters in institutional single-family homes do not qualify for a mortgage based on income or credit.

For these families, single-family rentals aren’t a luxury—they’re the only option.

There’s also evidence that the expansion of single-family rentals has increased racial and economic integration in certain neighborhoods by lowering the barrier to entry. Reducing this rental supply without replacing it with viable ownership paths could limit mobility rather than expand it.

What We Don’t Know (And That Matters)

The long-term effects of institutional ownership are still debated for one simple reason: the data weak or yet to come

There’s no consistent definition of “institutional investor.” Maybe a new regulation will define it.

New mindset, how many people really want to own a home vs keep renting?

After the 2008 crisis, these big firms helped stabilize neighborhoods by reducing vacancy—but today’s market is very different.

This shift is not about punishing investors. It’s about the well-being of families who are working, waiting, and still failing to access homeownership.

The data behind these decisions is extensive and still evolving. we need time to see the real impact, no doubt this conversation is just beginning. Stay tuned.

Related Realty support the principles of the Fair Housing Act (Title VIII of the Civil Rights Act of 1968), as amended, which generally prohibits discrimination in the sale, rental, and financing of dwellings, and in other housing-related transactions, based on race, color, national origin, religion, sex, familial status (including children under the age of 18 living with parents of legal custodians, pregnant women, and people securing custody of children under the age of 18), and handicap (disability). As an adjunct to the foregoing commitment, both RelatedISG Realty and Inside Real Estate actively promote, and are committed to, creating and fostering an environment of diversity throughout their respective organizations and franchise systems, and each views such a concept as a critical component to the on-going success of their business operations.

The opinions expressed herein do not necessarily reflect the views or standpoint of Related Realty. While the information provided has been researched and fact-checked using reputable sources, readers are encouraged to verify the accuracy independently. This material may include opinions and data relevant to a specific date, and market insights may change over time. Under no circumstances should any content be construed as legal, tax, or financial advice. The information is provided solely for reference and educational purposes.

All rights reserved @ 2025 Axel Ivan Gonzalez Cordido P.A.